Blockchain Technology Pros and Cons

In recent years, blockchain technology has gained popularity, presenting the potential to disrupt numerous industries. This article aims to outline the primary pros and cons of blockchain while also providing a detailed overview of the technology.

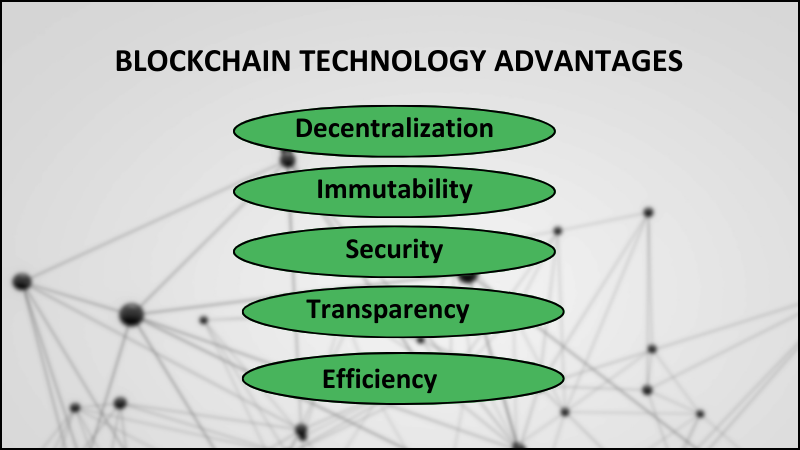

Blockchain Technology Advantages

- Decentralization: Blockchain removes the necessity for a central authority, enabling individuals and lessening dependence on trusted intermediaries. This encourages transparency, instills trust, and mitigates the risk of fraudulent activities or manipulation.

- Immutability: Once information is recorded on a blockchain, it becomes immutable and cannot be modified or erased. This guarantees the integrity and genuineness of data, establishing a dependable record of transactions.

- Security: Through cryptographic algorithms and distributed ledger technology, blockchain exhibits high resilience against cyberattacks and unauthorized access, enhancing security measures.

- Transparency: Every transaction conducted on a blockchain is visible to all participants, fostering accountability and minimizing the likelihood of corrupt practices.

- Efficiency: By automating procedures and removing middlemen, blockchain can streamline transactions, leading to time and cost savings.

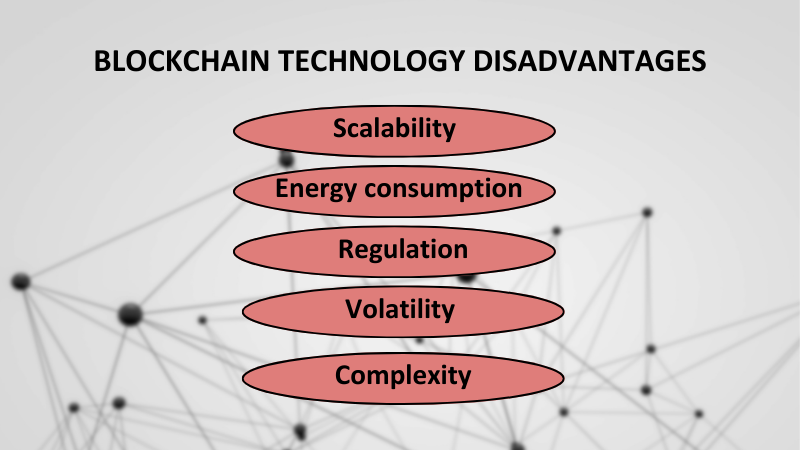

Blockchain Technology Disadvantages

- Scalability: Present blockchain technology may encounter difficulties in managing substantial transaction volumes, which could impede broader acceptance.

- Energy consumption: The utilization of proof-of-work consensus mechanisms in certain blockchains demands considerable computational resources, prompting concerns regarding environmental repercussions.

- Regulation: Ambiguity in regulations pertaining to blockchain contributes to uncertainty, potentially impeding innovative endeavors.

- Volatility: Cryptocurrencies linked to specific blockchains may undergo significant price fluctuations, presenting risks for investors and businesses.

- Complexity: Grasping and implementing blockchain technology necessitates technical proficiency, which might serve as a barrier for certain users.

Key Facts on Blockchain

Blockchain technology and cryptocurrency are two terms often used interchangeably, but they are not the same thing. Here’s a breakdown of the key facts about each:

Blockchain Technology

A distributed ledger technology that stores data across a network of computers, rather than a single server. This makes it highly secure and transparent.

Key features:

- Decentralization: No single entity controls the network, making it resistant to censorship and manipulation.

- Security: Cryptographic techniques and distributed consensus mechanisms ensure data integrity and prevent unauthorized access.

- Transparency: All participants have access to the ledger, fostering trust and accountability.

- Immutability: Once recorded, data cannot be altered or deleted, ensuring the accuracy of the historical record.

Cryptocurrency

A digital or virtual currency that uses cryptography for security. It operates independently of central banks and governments. You can also read about crypto FAQ.

Key features:

- Decentralization: No central authority controls the issuance or management of the currency.

- Security: Cryptographic techniques secure transactions and protect against counterfeiting.

- Transparency: Transactions are recorded on a public blockchain, making them auditable and transparent.

- Volatility: Cryptocurrency prices can fluctuate significantly, making them a risky investment.

What is Blockchain and How Does it Work?

Blockchain is a decentralized and distributed ledger technology that enables the secure recording and storage of transactions across a network of computers, known as nodes.

Unlike traditional centralized databases where data is stored in a single location controlled by a central authority, blockchain distributes copies of its ledger to all nodes in the network.

Here’s how it works:

- Transactions: Participants initiate transactions to transfer assets or data. These transactions are grouped together into blocks.

- Block Creation: Miners or validators in the network compete to solve complex mathematical puzzles to create a new block of transactions. This process is known as mining (in proof-of-work systems) or validation (in proof-of-stake systems).

- Consensus: Once a miner successfully solves the puzzle, the new block is verified and added to the existing blockchain by consensus mechanism in blockchain among the network participants. Consensus mechanisms ensure that all nodes agree on the validity of transactions and the order in which they are recorded.

- Immutability: Each block contains a reference (hash) to the previous block, creating a chain of blocks. This linkage ensures the integrity and immutability of the blockchain. Once a block is added to the chain, it cannot be altered or deleted without consensus from the majority of the network.

- Decentralization: Because the blockchain ledger is distributed across multiple nodes, there is no single point of control or failure. This decentralization enhances security, transparency, and resilience of the network.

- Verification: Every node in the network maintains a copy of the blockchain ledger and independently verifies the validity of transactions. This redundancy ensures that even if some nodes fail or act maliciously, the integrity of the blockchain remains intact.

What is Cryptocurrency and How does It Work?

Blockchain technology operates as a decentralized and distributed ledger system, where transaction records are stored across a network of computer nodes.

Transactions initiated by network participants are grouped into blocks, which are then validated and added to the blockchain through a process involving miners or validators solving complex mathematical puzzles.

This consensus mechanism ensures that all nodes agree on the validity of transactions and their chronological order.

Each block references the previous one, forming an immutable chain ensuring blockchain integrity and security.

Due to its decentralized nature, there is no single point of control, enhancing security and resilience.

Each node in the network holds a copy of the blockchain ledger and checks transactions independently, guaranteeing redundancy and integrity, which safeguards against failures or malicious activities.

Overall, blockchain technology facilitates secure, transparent, and tamper-resistant record-keeping across various industries without the need for intermediaries or central authorities.

Challenges and Opportunities for Blockchain Technology

Blockchain technology presents both challenges and opportunities as it continues to evolve and expand its applications.

Challenges

On the challenges side, scalability remains a significant issue for current blockchain platforms, which struggle to efficiently handle large transaction volumes, thereby limiting their scalability and adoption for widespread use.

Energy Consumption

Moreover, the energy consumption associated with proof-of-work consensus mechanisms, used in some blockchains like Bitcoin, raises concerns due to significant computational power requirements, leading to environmental sustainability issues.

Regulatory Uncertainty

Another challenge is regulatory uncertainty, as the lack of clear regulations and compliance standards surrounding blockchain technology creates ambiguity for businesses and investors, hindering its mainstream adoption.

Volatility

Additionally, the volatility of cryptocurrencies associated with blockchain technology poses risks for investors and businesses relying on them for transactions.

Flaws in Networks

Moreover, when different blockchain networks can’t easily communicate or transfer data, it holds back collaboration and innovation.

Opportunities

Despite these challenges, numerous opportunities exist for blockchain technology. Ongoing research and development efforts aim to address scalability issues through solutions like sharding, layer 2 protocols, and improved consensus mechanisms.

Innovations in consensus mechanisms, such as proof-of-stake and proof-of-authority, offer more energy-efficient alternatives to traditional proof-of-work systems, thereby reducing environmental impact and promoting sustainability.

Moreover, progressive regulatory frameworks and increased collaboration between industry stakeholders and policymakers can provide clarity and foster a conducive environment for blockchain innovation and adoption.

Advances in cryptographic techniques, secure multi-party computation, and decentralized identity management contribute to strengthening the security of blockchain networks, mitigating risks of fraud and cyberattacks.

Additionally, the development of interoperability standards and protocols facilitates seamless communication and data exchange between different blockchain platforms, unlocking new possibilities for cross-chain applications and collaborations.

Conclusion Blockchain Technology Pros and Cons

In summary, blockchain technology offers decentralized, secure, and transparent solutions with global accessibility.

However, challenges such as scalability, energy consumption, regulatory uncertainty, and complexity may hinder its widespread adoption.

FAQ

What are the advantages and disadvantages of the blockchain technology❓

Blockchain technology advantages offers security, transparency, and cost-effectiveness, but faces challenges such as scalability issues, irreversible transactions, energy consumption concerns, and complexity in understanding its workings.

What is blockchain technology❓

Blockchain is like a digital ledger that records transactions in a secure and transparent way. Instead of one central authority, it’s decentralized, meaning lots of computers keep copies of the same record.

How is blockchain used in real life❓

Blockchain is used in many ways. For example, in finance for cryptocurrencies like Bitcoin, in supply chain management to track products, and even in voting systems to ensure transparency and security.

Is blockchain technology suitable for every situation❓

Blockchain technology is not always the best solution for every problem. Its suitability depends on factors such as the need for transparency, security, and transaction volume, so it’s crucial to assess whether blockchain is the appropriate tool for the task at hand.

Is blockchain 100% safe❓

Blockchain technology offers strong security due to its decentralized nature, but it’s not 100% safe from all risks and vulnerabilities, so caution and good practices are still necessary.